PURCHASING PROPERTY ON TRUST FOR YOUR CHILD IN SINGAPORE

For individuals looking to purchase a second property as a form of investment or for legacy planning purposes, the Additional Buyers Stamp Duty acts as a huge deterrent. To circumvent the hefty costs of the cooling measures, some individuals have decided to purchase the property and hold it on trust for their minor children. However, it is important to understand the legal and tax implications of holding the property on trust.

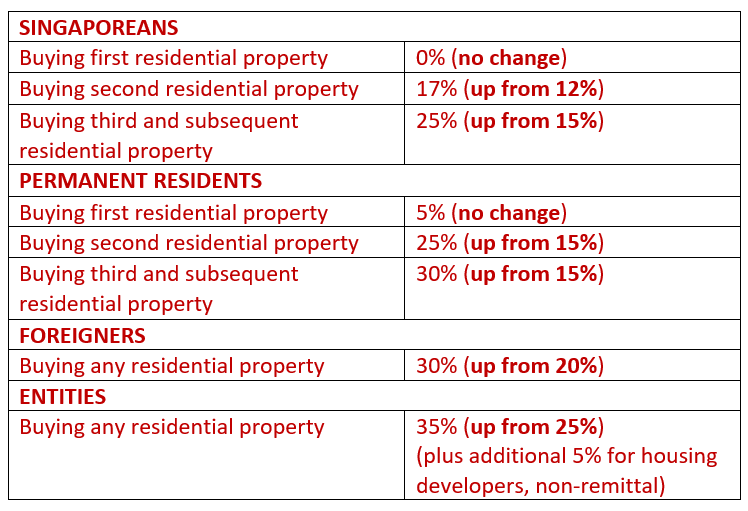

ABSD UPDATE:

ADDITIONAL BUYER’S STAMP DUTY RATES FROM 16 DECEMBER 2021

Amidst the Covid-19 pandemic situation, many individuals appear undeterred by the recent downturn in the economy and surge in job losses as Singapore saw a 36.3 per cent year-on-year increase in the sale of private homes by developers in September 2020.

In this regard, the Government does not appear to have any intentions of easing the latest cooling measures introduced in July 2018 i.e. the increase in the Additional Buyer’s Stamp Duty (ABSD) rates and the tightening of the loan-to-value (LTV) limits on residential property purchases.

Singaporeans planning on getting a second or subsequent residential property will have to pay an ABSD of 12% or 15% respectively. Against the backdrop of the increasing costs of investing in residential properties, some individuals have resorted to setting up trust to hold the residential property for the benefit of their children.

Regardless of the intentions of the settlor in setting up the trust, it is important to understand the implications of purchasing a residential property in Singapore via a trust arrangement, which goes far beyond any costs savings in terms of ABSD.

SEPARATION OF LEGAL AND BENEFICIAL OWNERSHIP

When purchasing a property through a trust arrangement, the legal and beneficial ownership of the property is divided such that the person appearing as the legal owner of the property (the “Trustee”) is different from the person who will be receiving the entire benefit of the property (the “Beneficiary”).

In other words, the Beneficiary will be reaping all the benefits from the trust e.g. income generated from the trust property will go to the Beneficiary, while the Trustee is charged with the task of managing the trust property and paying for the all related expenses and taxes.

Do note that a trust cannot be created over a HDB property unless written approval is sought from the HDB. If approval is not sought, the trust shall be deemed null and void.

Setting up an irrevocable trust bears several implications which property buyers should bear in mind:

Protection from creditors

Given that the property no longer forms part of the assets of the Settlor (i.e. the person who creates the trust), this means that property will be protected from any bankruptcy proceedings against the Settlor.

However, this protection is only afforded to the Settlor if the trust was set up more than 3 years before the commencement of bankruptcy proceedings[i]. If the trust was set up less than 3 years from the commencement of bankruptcy proceedings, then the Official Assignee may set aside the trust arrangement, and all necessary legal and tax implications will apply as though the trust was never set up.

In the same light, the trust property will also generally not be included into the pool of matrimonial assets that are subject to division in the event of divorce.

[i] See section 361 read with section 363 of the Insolvency, Restructuring and Dissolution Act 2018.

Irrevocability of trust

For irrevocable trusts, once the trust has been property established to hold the purchased property on trust for the Beneficiary, the property rightfully belongs to the Beneficiary.

This also means that if the Settlor has a change of heart and wants to reclaim the property, the Settlor cannot unilaterally revoke the trust. Such transfers will necessarily incur stamp duty, which is payable on the market value of the property.

For Settlors who are thinking of setting up a revocable trust to reserve some degree of control and interest over the trust property, it is forewarned that the Inland Revenue Authority of Singapore (IRAS) may likely take the view that the trust arrangement is a tax avoidance scheme, implications of which are discussed below.

TAX IMPLICATIONS

Buyers of a residential property in Singapore will have to pay Buyer’s Stamp Duty, as well as Additional Buyer’s Stamp Duty depending on the nationality and property count of the Buyer:

The property count of the Buyer is to be taken from the date of execution of the agreement to purchase the property, regardless of whether the property has been legally transferred to the Buyer.

The property count of an individual will include properties in which the Buyer has partial ownership or joint ownership. Where the Buyer i.e. Trustee purchases a residential property to be held on trust for the Beneficiary, the property will be counted under the Beneficiary’s property count.

Therefore, if the Beneficiary under the trust is a Singaporean citizen with zero residential properties under his or her name, ABSD is not payable even if the Buyer owns multiple residential property

Anti-avoidance rule under section 33A of the Stamp Duties Act

With that being said, if the authorities are satisfied on the evidence that the true intention of the trust arrangement is not to purchase the property for the benefit of the Beneficiary, but rather, it is solely to avoid ABSD with the intention of reaping profits from the trust property for the Buyer’s benefit, then the Commissioner of Stamp Duties may disregard the trust arrangement.

In such circumstances, ABSD will be payable on the trust property. Further, in light of the recent Income Tax (Amendment) Bill 2020, a surcharge equivalent to 50% of the amount of ABSD payable will also be imposed once the amendments take effect.

Trust Income

As stated above, all benefits arising from the trust property e.g. rental income, sale proceeds etc. will accrue to the Beneficiary.

For instance, if the trust property is rented out, the rental income will be held by the Trustee on trust for the Beneficiary, thereby constituting trust income.

Generally, where trust income is earned or received in Singapore, such income is deemed to be the statutory income of the trustee and is subject to income tax at a flat rate of 17%.

However, if the Beneficiary is a resident in Singapore, transparency will be accorded to the Beneficiary, and no tax will be imposed at the trustee level. Instead, the beneficiaries are subject to tax on their entitlement to the income and enjoy the concessions and exemptions that may be available to them.

On the other hand, any gains from the sale of the trust property in Singapore will not be taxable as it is a capital gain. However, such exemption will not apply where circumstances show that the trust is set up for “trading in properties” e.g. high frequency of transactions, short holding period of the properties etc.

In any event, the Beneficiary must declare his or her share of the income from the trust property in his or her individual tax returns as trust income when it is distributed to him or her.

PRACTICAL CONSIDERATIONS

One cannot simply ignore the practical implications of purchasing a property through a trust arrangement.

Financing the purchase of the property

Buyers will most probably have to be make upfront payment for the trust property as banks and financial institutions are unlikely to grant loans for properties purchased under the trust, especially if the Beneficiary is below the age of 21 and not working.

Implications on the Beneficiary

If the trust was set up for the benefit of the minor child i.e. to provide for the future needs of the minor child, then it is important to consider the implications of the trust on the child’s future property purchases.

For one, the child will not be eligible to purchase a HDB property, such as a HDB Build To Order (BTO) flat with his or her spouse. Even if the child were to sell the trust property, he or she will have to wait for another 30 months before being eligible to apply for a BTO flat.

For the purchase of a HDB resale flat, the child will have 6 months from the date he or she takes ownership of the resale flat to dispose of the trust property.

On the other hand, if the child intends to purchase another residential property in the future, he or she will be required to pay ABSD on his or her future property.

SETTING UP A TRUST

To set up a trust, a trust deed has to be executed between the Settlor and the Trustee. It is essential that the trust deed provides for the following key terms:

- the minor beneficiary(ies) under the trust;

- the powers conferred on the Trustee for purposes of administering the trust; and

- the termination of the trust.

The trust deed should provide a comprehensive set of powers to the Trustee to enable the Trustee to adequately manage the trust property for the benefit of the Beneficiary.

While the Trustees Act (Cap. 337) in Singapore does provide for certain powers such as a general power of investment and maintenance, the trust deed can provide greater guidance and restrictions on the scope of the Trustee’s powers, which will prevail over the powers provided under the Trustees Act in the event of a conflict.

Generally for a fixed trust, the trust may be terminated and the legal title of the trust property will be passed on to the child Beneficiary from the Trustee if the Beneficiary attains the age of 21 and is absolutely entitled to the property based on the terms of the trust.

At Infinity Legal LLC, we advise and help individuals set up a trust arrangement to manage their assets and provide for their legacies.

© Infinity Legal LLC 2020

For PDF version of this article, please click here.

The content of this article is for general information purposes only, and does not constitute legal advice and should not be relied on as such. Specific advice should be sought about your specific circumstances. Infinity Legal LLC does not accept any responsibility for any loss which may arise from reliance on information or materials published in this article. Copyright in this publication is owned by Infinity Legal LLC. This publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.